The Pigou effect was introduced by Arthur Cecil Pigou in 1943 in his article “The Classical Stationary State,” published in the Economic Journal. In this work, Pigou suggested a connection between “real balances” and consumption. You can read more about History of Pigou Effect below.

In classical economics, Pigou liked the concept of “natural rates,” which he believed the economy would usually return to. However, he recognized that sticky prices could stop this return after a demand shock. Pigou viewed the real balance effect as a way to connect Keynesian and classical theories. According to this effect, when purchasing power increases, government spending and investment tend to decrease.

Critics of the Pigou effect argue that if it consistently worked in an economy, the very low nominal interest rates in Japan during the 1990s should have ended the long-lasting deflation there more quickly than it actually did.

One clear sign against the Pigou effect in Japan is the long period of low consumer spending while prices dropped. Pigou argued that lower prices should make people feel wealthier and encourage them to spend more. However, Japanese consumers chose to wait, hoping prices would decrease even more.

Critique of the Pigou Effect

The Keynes Effect suggests that when prices decrease, a fixed amount of money will have more purchasing power, leading to lower interest rates. This encourages businesses to invest and spend more on physical assets, which helps the economy grow. Essentially, it means that lower prices can help fix problems of low demand and production.

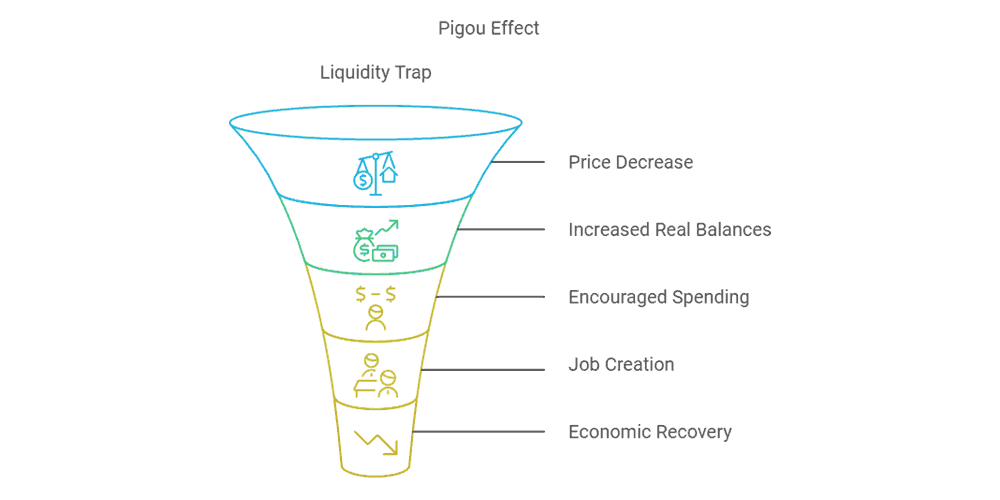

The Pigou Effect explains that when real balances increase, aggregate demand decreases. If prices drop, people have more money to spend, leading to higher spending due to the income effect.

If this were true and the Pigou effect always worked, then the Bank of Japan’s low interest rates would have effectively tackled deflation in the 1990s. However, the steady spending in Japan, even with falling prices, contradicts the Pigou effect. Japanese consumers expected prices to drop further, so they postponed their purchases.

Government Debt & Pigou Effect

Robert Barro, an economist from Harvard, argued that because of Ricardian equivalence, people cannot be misled into believing they are wealthier when the government sells them bonds. This is because the government must cover bond payments by raising taxes in the future. Ricardian equivalence is a theory that suggests whether the government funds its spending through current or future taxes, the impact on the economy remains the same. Barro claimed that at the individual level, the perceived wealth should decrease when the national government takes on part of the debt.

Bonds should not be seen as part of total wealth in the economy. This means, he argued, that a government cannot create a Pigou effect by issuing bonds since the overall wealth will not rise.

Pigou Challenge

Pigou argued against the free market by proposing that the government should step in and tax businesses and people for the harm they cause to society. He thought that those who pollute should pay taxes and that health insurance should be mandatory.